Place-based vulnerability to cost of living pressure

Where we are and where we’re headed

Kristina Stipetic

Research Analyst

Kristina Stipetic

Research Analyst

In 2022, the Centre for Progressive Policy released an index ranking every local authority in England against its vulnerability to what was then called the cost of living crisis. Nearly four years on and the cost-of-living struggle, far from receding, has only become more entrenched. There has been no overall progress on poverty in last decade, and the number of families with children in poverty have increased since 2020. The median household disposable income has remained stagnant since the pandemic. Looking beyond purely monetary indicators reveals a wider sense of discontent - people feel the economy isn’t working for them: 76% of Britons described the economy as “poor” in October 2025. But even this may seem like a sunny outlook compared with the storm following America’s attack on Iran, which has caused the already-increasing cost of living to rise to even greater heights.

Fuel prices have already begun to rise, with Brent crude increasing over 40% since the beginning of 2026. Household energy bills will likely feel the impact in autumn, as the government has capped prices until July.

Food prices will be hit via two channels: first, the increased cost of transport due to rising petrol prices and the second, the cost of fertiliser. Nitrogen-based fertiliser, which is used to grow most crops, requires a large amount of gas to create. Combined with the fact that the UK imports most of its fertiliser from the Middle East and North Africa, where shipping is currently disrupted, means that the war could not have come at a worse time for farmers.

Inflation, which was predicted to decrease before the war, is now holding steady at 3%, and some analysts warn that it could reach 4.6% by the end of this year. This latest chapter in the cost of living struggle may turn out to be the most intense one yet, and, as with previous, places will feel the effects differently.

To identify patterns in vulnerability and help local and combined authorities set priorities in the face of mounting pressures, the Growth and Reform Network have recalculated the cost of living index with the latest data. Today, we share our research in the form of three key findings:

- Vulnerable places stayed vulnerable

- Coastal areas are more vulnerable

- Child poverty and claimant count are stable, while low pay and economic inactivity are volatile

The most vulnerable places remain vulnerable

The landscape hasn’t changed much since 2022. Members have confirmed that the story they were expecting is the story told by our data: vulnerable places have stayed vulnerable.

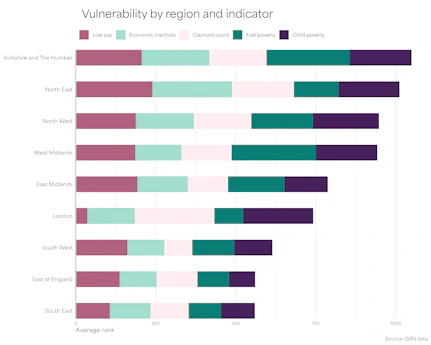

We found that the populations of Sandwell, Blackpool, Birmingham, Blackburn and Darwen and Nottingham are most vulnerable to the rising cost of living. All five of these places are also ranked in the top decile of the Index of Multiple Deprivation, meaning that they suffer from a set of complex, interconnecting disadvantages. Regionally, there are high concentrations of vulnerable places in the North West, West Midlands, and Yorkshire and the Humber, each with a slightly different mixture of challenges. The West Midlands struggles with fuel poverty, while the North East stares down the dual nemeses of economic inactivity and low pay.

Five local authorities in our top decile (Leister, Thanet, Luton, Stoke-on-Trent, and Telford and Wrekin) are currently not on any devolution pathway, highlighting the potential for places to slip through the cracks if they aren’t integrated with a specific devolutionary path.

Coastal areas are more vulnerable

We found that coastal areas are more vulnerable, on average, than other area types, a trend that was also evident in the previous Index. Coastal areas also show similar patterns to one another across England. For example, although the South East is the least vulnerable region overall, its coastal regions - Thanet and Hastings - rank in the upper decile of vulnerable places, with high instances of low pay and economic inactivity.

There are a few reasons for coastal areas’ particular vulnerabilities. Young people struggle to find work due to a confluence of factors, including poor transport infrastructure and lack of youth support. Poor transport links and broadband coverage are major obstacles for these communities trying to move their economies away from hospitality. Local authorities’ funds are stretched due to the challenge of defending coastal communities against harsh weather, flooding, and erosion. Combined with severe underfunding from national government, and the suspension of EU structural funding, councils have little money left to invest in desperately needed public services.

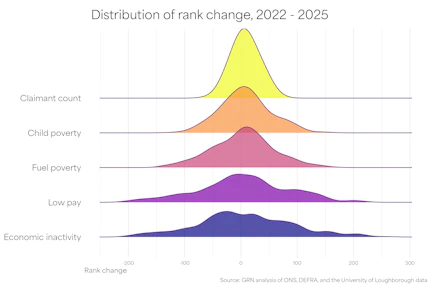

Child poverty and claimant count are stable, while low pay and economic inactivity are volatile

In the three years between 2022 and 2025, the proportion of people claiming benefits and the proportion of children in poverty did not change that much.

Child poverty is entrenched in certain places and disconnected from improvements in pay and employment at the local authority and regional level.

On the other hand, levels of low pay and economic inactivity fluctuated dramatically with no clear regional pattern. Some neighbouring local authorities, such as North and Mid Devon, swung sharply in opposite directions. Some of the fluctuation may be explained by central government investment, for example Erewash – an urban local authority in the East Midlands - lowered economic activity from 25.9% in 2022 to 11.8% in 2026. In 2022, Erewash successfully bid for £2.5 million of the UK Shared Prosperity Fund which it invested in its economic development. However, not every fluctuation can be explained this way and the topic requires further investigation.

Conclusion

In January 2026, the government published its Crisis and Resilience Fund guidance for local authorities. The fund, which is the first ever of its kind, aims to support low-income families struggling with sudden or unexpected financial burdens such as disasters and health emergencies. The recent announcement promising targeted help with energy bills in response to the war is also welcome. However, persistent vulnerability requires sustained investment as well as flexible reactive funds. The greatest hope for this kind of change is the roadmap on fiscal devolution, due to be released in the Northern Growth Strategy in Autumn, which proposes to pass a share of the national tax revenue to mayors, thereby allowing them to proactively address the unique mixture of infrastructure and economic issues that render their areas vulnerable to shocks. With this increase in devolved powers, we hope to see stronger place-based resilience and an eventual reversal of the rising costs of living.

GRN articles and insights

Browse other GRN articles and insights in inclusive growth and public service reform across the UK: